Good Morning Nonprofits!

We hope you are all doing well and staying safe! We found this very helpful article in Community Brands Knowledgebase and thought it was very important that you see this if you're having issues with dealing with sick leave during this hard time.

- From the Desk of Jeron Comeau

Question: On March 18th the Federal Government Passed HR 6201. This legislation qualifies many workers for up to 80 hours of sick leave and the government will reimburse employers for this expense. What is the best way to set this up in MIP?

Answer:

NOTE: This is a developing issue subject to change by the interpretation from government agencies as well as additional legislation under consideration. The information in this KB may change as things develop. These instructions are intended to allow customers to record as much information as possible in anticipation of future reporting requirements. This is not the only way to set these things up or record the information.

You should consult your HR/Tax advisor before paying anyone money or reducing your tax remittance to make sure you are in compliance.

Background: HR6201 contains many provisions for providing relief and assistance for workers and businesses affected by COVID-19 that have fewer than 500 employees. There are two programs. A sick leave program and an extended leave program. For payroll customers there are several key provisions.

The Sick Leave Program

1 – Allowing that workers affected by COVID-19 who are personally sick or under quarantine receive up to 80 hours of paid sick leave. The government will reimburse employers for this expense via deductions and or credits to payroll taxes.

2 – Allowing that workers who must care for someone who is affected by a COVID19 quarantine or care for a child whose school/care facility is closed because of COVID19 to receive up to 80 hours of paid sick leave at 2/3 pay.

The Extended Leave Program

3 – If workers must care for children whose school/care facility is closed because of COVID19 beyond the initial 80 hours of out of the sick leave program at 2/3 pay they may in some instances receive up to an additional 10 weeks of expanded FMLA at 2/3 pay.

In addition to the above eligible employers are entitled to an additional tax credit determined based on costs to maintain health insurance coverage for the eligible employee during the leave periods above.

NOTE: There are certain exemptions, exceptions and limits on who qualifies for this and how much can be reimbursed per employee for each of the items above. You should consult with your Tax/HR advisor about who qualifies and what these limits are.

In all the above scenarios the qualified sick leave amounts will be paid to the employee by the employer and then the employer will be reimbursed by the government. This reimbursement will be in the form of a reduction in the amount of payroll taxes remitted to the government. If the amount of qualified reimbursements is greater than the payroll taxes the employer remits to the government, the government will issue the employer a refund.

Setup In MIP

Because the expense for these provisions will be reimbursed by the federal government it is desirable (but not required) to track it separately from normal sick leave and sick leave expense. For tracking purposes, it is easiest to set up separate codes for each of the scenarios. It is best to set up both an earnings code and a leave code for each of the programs. Such codes might be:

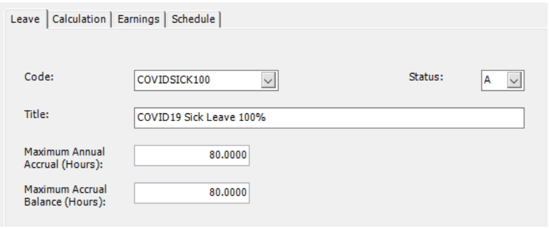

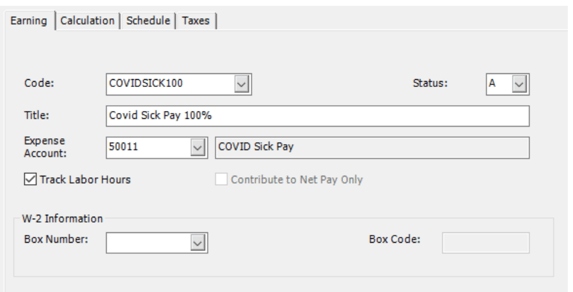

COVIDSICK100 – Used for provision 1 where an employee is personally sick or under quarantine using the 80 hours of sick leave at 100% of pay.

COVIDSICK2/3 – Used for provision 2 where an employee is using sick leave to take care of someone or their children using the provided 80 hours of sick leave at 2/3 of pay.

COVIDLEAV2/3 – Used for provision 3 where the employee is taking care of children under the extended FMLA 10 week program at 2/3 of pay.

Provisions for reimbursement of insurance expenses would not be handled through payroll.

For each of these provisions you would set up both a leave code and an earnings code.

So you would have a leave code called COVIDSICK100 and an Earnings Code called COVIDSICK100. In the case of the COVIDSICK100 and COVIDSICK2/3 leave codes you may wish to add a balance of 80 hours to track how much the employee has used on that balance for reporting purposes. Since the COVIDLEAV2/3 does not have a set number of hours you may wish to record hours used but not necessarily set hours for the employee to use for the future.

Setting up the Leave Code

Go to Maintain>Payroll>Leave Codes.

- Create a new Leave Code.

- Set the Maximum Annual Accrual and Maximum Accrual balance to be 80 hours.

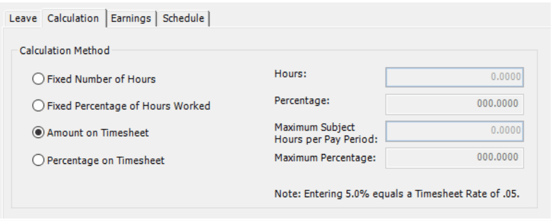

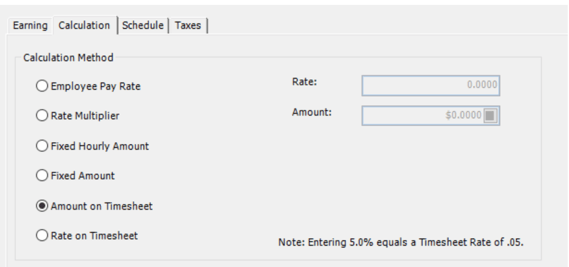

- On the Calculation Tab choose the Amount on Timesheet option. This means that when entering timesheets, you will need to put in the amount of leave taken each time. This gives maximum flexibility.

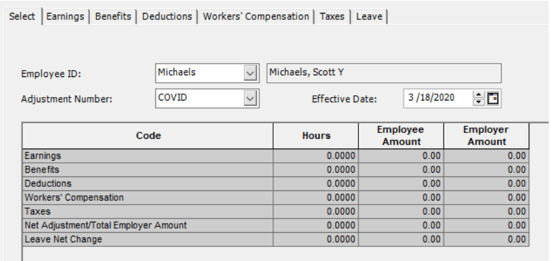

- If you wish to track how much of the allotted leave the employee has used then you will need to do an adjustment to put the leave balance in. Go to Activities>Payroll>Setup/Adjust Employee Balances. Select the employee and the effective date of the adjustment

- Go to the Leave tab and put 80 hrs. accrued. Click update. Repeat this for each employee affected

For HR Management users Only

In addition to using Setup/Adjust Employee Balances to add leave hours to an employees’ balance, you may also consider using the HR Mass Update feature. This tool allows HR Management users to adjust leave balances for multiple employees. Please reference, KB 22746 from www.abila.com for more detail on how to use HR Mass Updates.

Creating specific earnings codes

It is not technically necessary to use a separate earnings code to track COVID19 sick and leave pay, but it will make the accounting for the reimbursements easier.

- Go to Maintain>Payroll Earnings Code. Create a new earnings code. When creating this earnings code attention should be paid to what GL code these expenses will flow into. These expenses and their distribution will in theory be a wash when the government reimburses employers or when you reduce this expense by moving money from the various payroll liability accounts. It may be helpful to have the amount of COVID19 Sick pay in its own GL account to simplify reporting, but it is not required. You could continue to use your regular salaries expense account if desired.

- On the Calculation Tab you will choose the calculation method. The method chosen depends on your needs, but Amount on Timesheet provides the most flexibility. It will require that everyone’s timesheet be updated. If you are using HR/EWS it also will allow those timesheets to flow. But what method you use is up to you.

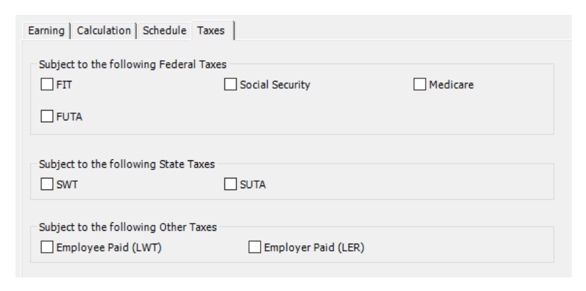

- On the Taxes tab check uncheck all the boxes. COVID earnings are not subject to tax.

When doing payroll, you can use the new COVID codes. On the earnings code you will need to choose a distribution code to go with it. Since the all of these expenses will be reimbursed by the government the distribution code doesn’t matter. However, to keep the coding simple it is recommended that you create a new COVID19 distribution code and distribution 100% to a specific code combination that will be easy to report on.

By setting up unique codes for COVID you can easily track how much sick leave is taken and the expense of that sick leave. If you have selected a Unique GL expense account in the earnings code setup it will make it easy to separate this expense from your regular payroll.

Reporting and Reimbursement

The government has indicated that it will reimburse employers for COVID related sick pay and extended leave pay. The mechanism of this reimbursement is supposed to be a credit to payroll taxes. If the amount of reimbursement exceeds the amount of payroll taxes paid the government is supposed to send refunds to employers.

For example if an eligible employer paid $5,000 in sick/extended leave and is otherwise required to deposit $8,000 in payroll taxes, including taxes withheld from all its employees, the employer could use up to $5,000 of the $8,000 of taxes it was going to deposit for making qualified leave payments. The employer would only be required under the law to deposit the remaining $3,000 on its next regular deposit date.

If an eligible employer paid $10,000 in sick/extended leave and was required to deposit $8,000 in taxes, the employer could use the entire $8,000 of taxes in order to make qualified leave payments and file a request for an accelerated credit for the remaining $2,000.

How this reduction in payroll taxes is to be reported and how any credits to taxes when sick/extended pay exceeds payroll taxes has yet to be determined by the government. Until that decided employers will continue to remit payroll taxes to the government normally. This KB will be updated as more information becomes available, but at the time of writing no decisions have been made.

Due to the nature of the payroll module it is unlikely that the recording of these reductions or credits for sick leave expense will be done through the payroll system. While no determination has been made it is likely that the actual accounting entries will be done in accounting via a JV or Cash Receipt. This is where using a separate GL account can be useful to more easily view and record these transactions.

If the amount of COVID19 Expense does not exceed the amount of payroll taxes the transaction might look something like this:

GL Debit Credit

Tax Liability X

COVID Expense X

If the amount of COVID19 Expense exceeds the amount of payroll taxes and the federal government reimburses the employer, then the transaction might look something like this:

GL Debit Credit

Tax Liability X

Cash X

COVID Expense X

Additional Information:

Q: How will I report this reduction in payroll taxes to the government? Will the form 941 be changed?

A: Guidelines about how these reductions are to be handled have not been set by the government yet. It has not been determined if they will be done via the 941. If the 941 is changed then Aatrix will release an update to the 941 and Abila will evaluate if we need to make changes to our payroll system to support that.

Q: If an employee has regular sick leave do they have to use it first before they can use this COVID leave? Can they be used concurrently?

A: You would need to consult your payroll/HR advisor about what type of leave can be used in which order. Additional clarification may come from the government.